Senate Finance Committee Press Release

Crapo, Wyden Issue Discussion Draft to Improve IRS Administration

On January 30, 2025, a discussion draft of the Taxpayer Assistance and Service (or “TAS”) Act was jointly released by Senator Mike Crapo, chairman of the Senate Finance Committee, and Senator Ron Wyden, the Committee’s ranking member. The TAS Act is a broad and sweeping bill aimed at improving tax administration. Of the 68 provisions, about 40 of them reflect legislative recommendations that I have made in my current and past Annual Reports to Congress and Purple Books. I previously discussed the significance of this potential legislation in terms of enhancing taxpayer rights. In upcoming blogs, I will highlight some of the provisions which, if ultimately enacted, will make great improvements in tax administration and help protect and strengthen taxpayer rights. This blog highlights the proposal to expand the Tax Court’s jurisdiction to allow taxpayers to bring refund suits in the Tax Court. As a former litigator, I understand the significance of this change for many low-income taxpayers and small businesses. It will make the difference of pursuing litigation or being forced to walk away from contesting the merits of an IRS adjustment.

Taxpayers have various rights, including the right to challenge the IRS’s position and be heard and the right to appeal an IRS decision in an independent forum. One of the provisions that I am most passionate about, which would streamline taxpayers’ right to judicial review of adverse IRS determinations, is Section 310 of the TAS Act, Authorization of Tax Court to Hear Refund Suits. This provision would expand the Tax Court’s jurisdiction, thus allowing taxpayers to file refund suits with the Tax Court. This provision is consistent with my 2025 Legislative Recommendation #43 and would be a game-changer for taxpayers.

Under current law, taxpayers cannot file a suit for refund in the Tax Court unless the IRS has determined that they owe additional tax and issued a notice of deficiency. This means that if taxpayers are only trying to get the IRS to refund tax they already paid, they cannot ask the Tax Court to review their claim. Instead, they must sue for a refund in either a U.S. district court or the U.S. Court of Federal Claims. Litigating in these courts is generally more challenging as the rules are more formal and less user-friendly, the filing fees are more costly, the judges generally do not have tax expertise, and proceeding without a lawyer is difficult. As a result, taxpayers often forgo pursuing litigation and lose refunds to which they may be entitled.

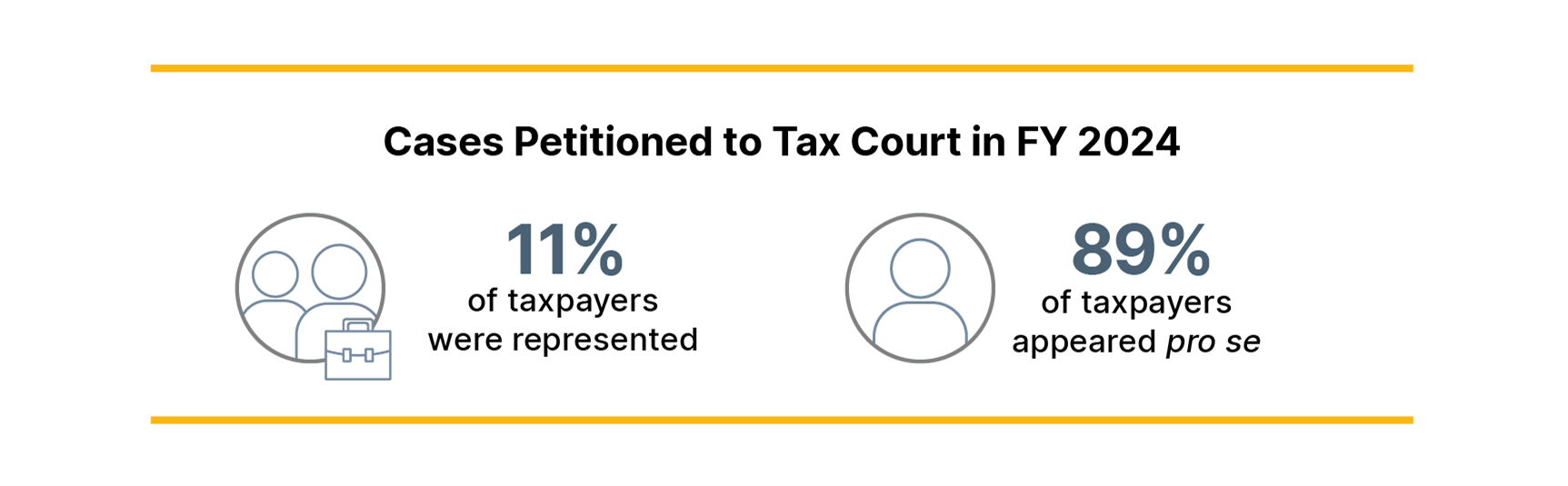

For most taxpayers, the Tax Court is the best forum in which to challenge IRS decisions. Due to the expertise of its judges, the Tax Court is often better equipped to consider tax controversies than other courts. It is also more accessible for average taxpayers because it has simplified informal procedures in disputes that do not exceed $50,000. For this reason, many taxpayers are able to represent themselves. Another benefit is that there are pre-existing programs within the Tax Court for low-income taxpayers to receive free legal assistance from a Low Income Taxpayer Clinic (LITC) or pro bono representation. The Tax Court is also significantly less expensive than district courts, with a filing fee of only $60, which can even be waived if taxpayers establish an inability to pay. In most instances, the Tax Court is the least expensive and best forum for low-income and smaller business taxpayers to get their day in court. In fiscal year (FY) 2024, about 97 percent of all tax-related litigation was adjudicated in the Tax Court and in FY 2024, 89 percent of taxpayers did not have representation before the court.

The positive impact of this potential legislation on taxpayers cannot be overstated. It would allow more taxpayers access to affordable litigation which they might otherwise forgo. For example, assume a taxpayer filed their return and reported $10,000 of tax due, which they paid in full. The taxpayer later discovers they made an error on the tax paid, and files a claim for a refund of the $800 they overpaid. If the IRS either denies or does not timely respond to the claim, under current law the taxpayer’s only option to challenge the IRS is to bring a refund suit in federal district court or the claims court. However, incurring the costs of a lawyer and higher court fees would most likely not make economic sense and many taxpayers may simply give up on getting a refund to which they might be entitled. If Section 310 of the TAS Act is enacted, taxpayers could proceed in Tax Court pro se for only a $60 filing fee, making challenging the IRS in court easier and more affordable, thus protecting their rights.

Enactment of Section 310 of the TAS Act would be a game-changer for everyone, especially lower-income taxpayers and small businesses. By expanding the Tax Court’s jurisdiction to hear refund cases, Congress would enhance taxpayers’ rights to bring actions that might otherwise be effectively denied and give all taxpayers a better opportunity to obtain judicial review of adverse IRS liability determinations. Our judicial system should not be limited to only those taxpayers that can afford to hire a lawyer to litigate the merits of their claim in the district court or claims court. Access to our justice system is a fundamental right we have as citizens. Taxpayers should not be deprived of their day in court due to cost challenges.

This legislative change would level the playing field for those wanting judicial review of their refund claims where the taxpayer might not be able to afford proceeding in district court or claims court.

The views expressed in this blog are solely those of the National Taxpayer Advocate. The National Taxpayer Advocate presents an independent taxpayer perspective that does not necessarily reflect the position of the IRS, the Treasury Department, or the Office of Management and Budget. NTA Blog posts are generally not updated after publication. Posts are accurate as of the original publication date. Portions of this blog may have been developed with the assistance of artificial intelligence. All AI-assisted content has been reviewed, verified, and approved by the National Taxpayer Advocate or TAS staff to ensure accuracy and integrity.